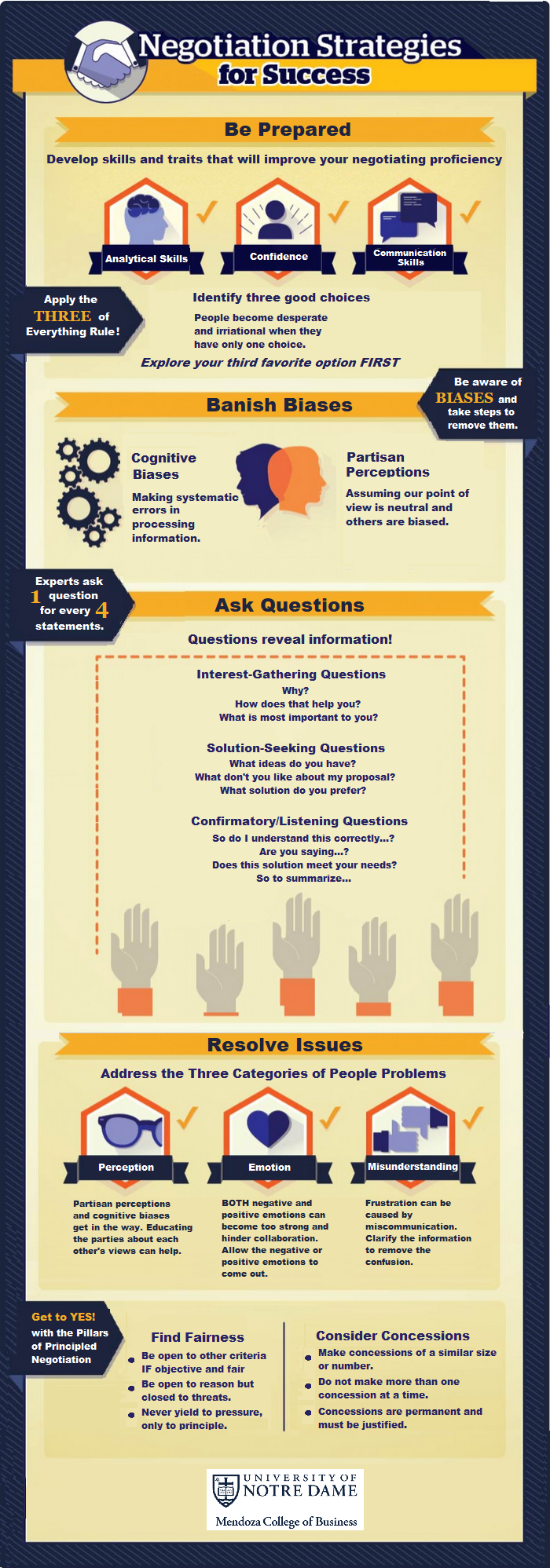

Mastering the Art of Negotiation

Tips to Improve Your Debt-Resolution Skills

Negotiating with people who owe you money, whether patients or other consumers, is not an exact science – it's an art.

You won't find a mathematical formula that works for every scenario. Successful negotiators always create a strategy but don't rigidly adhere to a predetermined plan. Instead, they remain flexible. Here are a few guidelines to consider when negotiating debt repayment with a consumer.

Research, Then Identify

Familiarize yourself with the facts about the account. conduct some internal research to be prepared to discuss the situation completely.

Learn to Recognize Stallers

Can you recognize when a debtor is stalling and has no intention of paying an overdue account balance? Here are some signs to look for:

- The consumer ignores phone calls, emails, and letters, or their voicemail greeting claims they're always on vacation. You're being ghosted.

- The consumer alleges a minor cost discrepancy in an attempt to hamper the collection process and escape paying the bill.

- The consumer deflects blame by claiming they never received the invoice or they already sent payment.

The best strategy for handling stallers is the three-strike rule: If they offer excuses on three or more occasions, send the account to collections.

After researching the account, you'll be in a better position to identify the overdue consumer as one of three types:

- Intends to pay

- Wants to pay but is not yet able

- Does not intend to pay

Listen to Find Out Why

How did this collection situation get out of control in the first place? Sometimes, simply asking the consumer about what went wrong, you'll learn that it's only a temporary problem or that help is on the way.

If so, you could structure a moratorium to help the consumer get through the rough patch before resuming regular payments. By understanding what went wrong in the first place, you can help find the best solution.

Actively listen to the consumers who want to pay you and strive to understand their personal circumstances. Allow them to air any grievances they may have. Doing so will help build trust and optimize your chances for recovery.

Negotiate as Equals

Treating the consumer as an equal will make them far more amenable to working with you. To find some common ground for negotiation, you must establish a level of respect.

Begin by asking the debtor to suggest terms that would work for them. If the proposal is unacceptable, counter the offer by suggesting a substantial down payment followed by monthly payments for the remainder.

For example, suppose the consumer offers to pay $25 monthly to cover a $500 debt, but your company's guidelines would consider such an offer unsatisfactory. In that case, it's up to you to turn the proposal into an acceptable arrangement.

You could offer to accept $50 monthly over six months if the consumer makes a $200 good-faith payment now. The consumer may either accept your offer or counter with payments of $40 per month instead. Either way, the negotiation is now moving in the right direction. Always work toward higher payments over a shorter term, but remain flexible.

Confirm and Finalize

Once you reach an agreement with the consumer, committing the terms to a written contract signed by both parties improves your chances of successful debt resolution.

After the consumer has remitted the first payment, end the conversation on a positive note. Reassure them that the payment arrangement places their account back in good standing with your organization.

At the same time, you also want to clarify the ramifications of failing to abide by the agreement. Tell them their account will be referred to collections if they breach the terms. This is your trump card -- one you must adhere to, no matter what relationship you have developed with the debtor.

--Article Continues Below--

Send in the Pros

If you've reached a stalemate in your negotiations with a past-due customer or patient, it's time to call in the professionals.

At CBSI, our collection professionals are skilled negotiators. Working within your organization's approved parameters, we maximize debt recovery by employing preparation, empathy, and creative problem-solving techniques. Contact us.

Recent Posts

Share On: